From Hype to Hard Reality: Enterprise AI in 2026

Introduction

Two years ago, I asked a simple question:

Is Generative AI truly being adopted inside enterprises — or are we mistaking hyperscaler investment and market excitement for real transformation?

In 2026 the conversation has only intensified. Big Tech continues to invest heavily in AI infrastructure. Governments host global AI summits. Media narratives swing between extremes — one day AI will transform every industry overnight, the next day software is declared dead and millions of jobs are predicted to disappear.

Inside most enterprises, the reality is more measured.

Boards are asking how AI initiatives connect to customer value, cost structure, risk, and durable revenue. Executive teams are being pushed to show measurable outcomes — not just pilots, prototypes, or proofs of concept.

A small group of organizations is beginning to translate AI experimentation into real operational impact. Many others remain in pilot mode, navigating integration challenges, governance questions, and organizational readiness.

Much of today’s debate is shaped by powerful narratives:

- Software is dead and AI agents will replace enterprise applications.

- Big Tech is investing heavily in AI infrastructure in anticipation of rapid enterprise adoption.

- AI will eliminate large numbers of jobs in the near term.

- AI is already destroying entry-level opportunities for recent college graduates.

Each narrative contains elements of truth. But technology transitions rarely unfold as quickly or as uniformly as the headlines suggest.

Much of what we hear about AI today is directionally correct — but chronologically wrong.

In the sections that follow, I examine where Generative and Agentic AI stand today, how enterprises are translating AI into business use across industries and functions, why pilots often stall before scaling, and why several widely repeated narratives deserve closer scrutiny.

Overview of Generative AI and Agentic AI

Before discussing adoption and impact, it helps to clarify terms.

Generative AI refers to systems that create content — text, images, code, audio, or video — based on patterns learned from large datasets. A user provides a prompt, and the system generates a response.

Over the past three years, enterprises have used Generative AI primarily as a productivity layer — drafting documents, assisting development, summarizing reports, and improving knowledge workflows. The model responds; the human directs.

In 2026, the focus has shifted toward Agentic AI.

Agentic AI goes beyond generating answers. It refers to systems designed to pursue a goal — often across multiple steps — with limited human intervention. Instead of simply responding to prompts, these systems can plan, take actions, interact with tools, retrieve information, and adjust based on outcomes.

If Generative AI helps you write an email, Agentic AI attempts to complete the task the email was meant to initiate.

This shift has fueled much of the current excitement. Open-source projects such as OpenClaw gained rapid attention by demonstrating early autonomous task workflows. Despite initial instability and hacks, the speed of innovation was notable. When its founder was quickly recruited by OpenAI, it signaled something important: major players see long-term strategic value in agent-based systems.

That does not mean enterprises are fully autonomous. Most implementations remain supervised and experimental.

Adoption trends across industries and business functions

The public narrative suggests rapid and universal acceleration. The data suggests something more structured — and more predictable.

Over the past three years, Wharton’s Human-AI Research in collaboration with GBK Collective has tracked familiarity and expertise in Generative AI across industries and functions. The trend is unmistakable: awareness and self-reported expertise have risen steadily year over year.

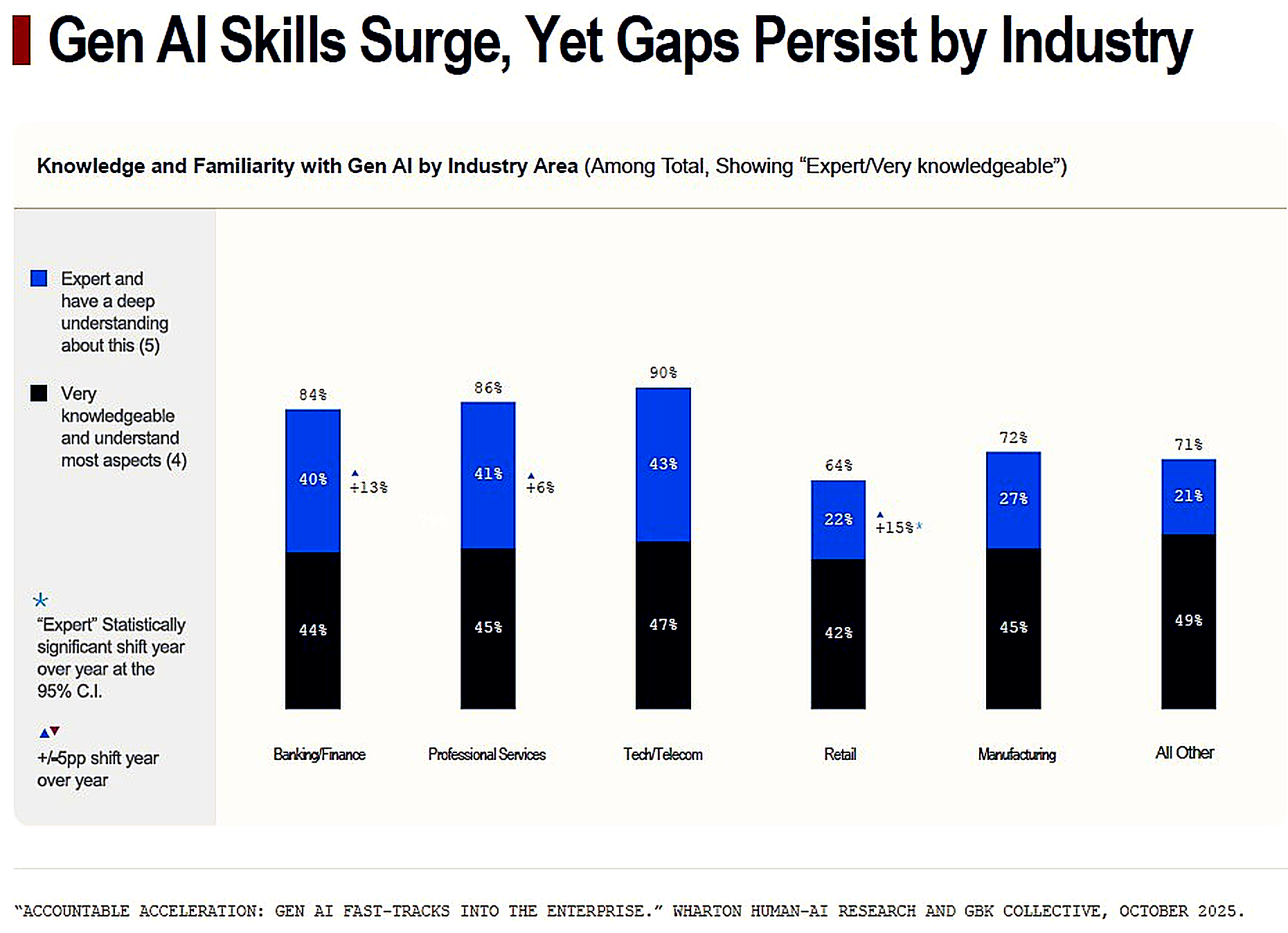

Industry Patterns: Progress, But Not Uniform

Technology and telecom continue to lead in deep familiarity with Generative AI. Professional services and banking follow closely. Retail and manufacturing show improvement across the three-year period, though they remain behind the digital-first sectors.

Source- Wharton Human-AI Research & GBK Collective (2025). Accountable Acceleration: Gen AI Fast-Tracks into the Enterprise. Page 18

This divergence is not surprising. Industries that are already software-centric tend to experiment earlier and more aggressively. Capital-intensive and operationally complex industries move more deliberately, balancing innovation with integration, compliance, and workforce retraining.

Srinath Nagarajan, a seasoned banking innovation and product leader says

“Financial institutions are balancing innovation and risk with the speed at which customers are ready and willing to adopt the benefits of new technologies. To get to these new end zones faster, progressive firms are focusing on talent by both investing in internal talent and recruiting leaders from non-banking firms.”

“History will show us that those who make definitive investments in capabilities and talent today will reap the rewards for time to come. Those who wait by the sidelines will find it harder to play catch up and lead the pack.”

The trajectory is upward across the board. The starting points, however, are different — and that difference shapes pace.

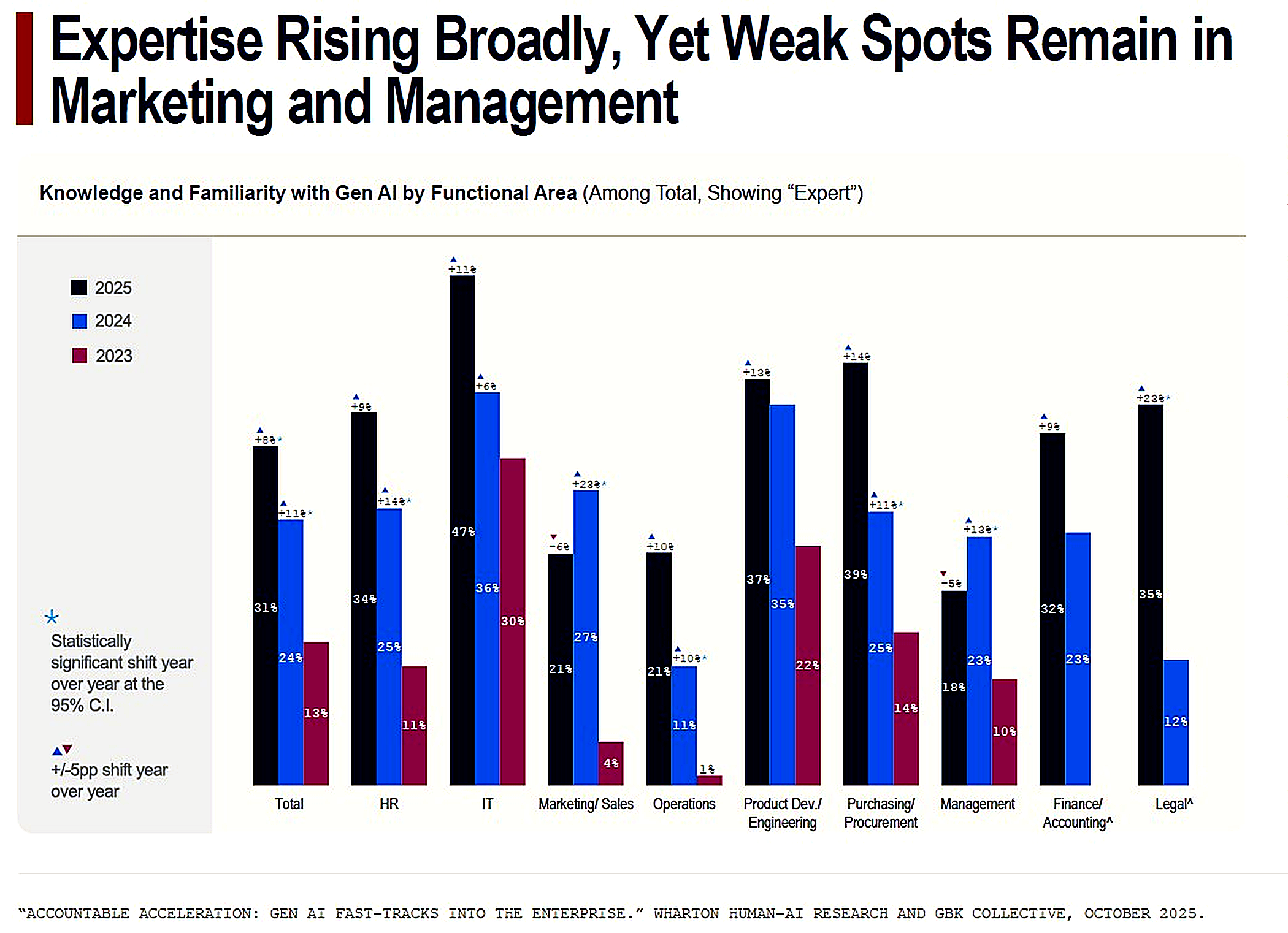

Functional Readiness: Strength in Some Areas, Gaps in Others

A similar pattern appears when examining business functions.

Source- Wharton Human-AI Research & GBK Collective (2025). Accountable Acceleration: Gen AI Fast-Tracks into the Enterprise. Page 17

Over the same three-year period, expertise growth has been strongest in IT, legal, procurement, and product development. These areas operate close to structured data, documentation, and analytical workflows — natural environments for early Generative AI adoption.

Marketing, sales, and general management show slower growth in deep familiarity. That gap matters. Strategic direction and capital allocation often sit within these functions. When understanding is still maturing at the decision-making layer, scaling tends to proceed cautiously.

Capability is spreading. It is simply not embedded evenly across influence centers.

Agentic AI: Ambition Exceeds Broad Deployment

When attention shifts from Generative AI to Agentic AI, the contrast becomes clearer.

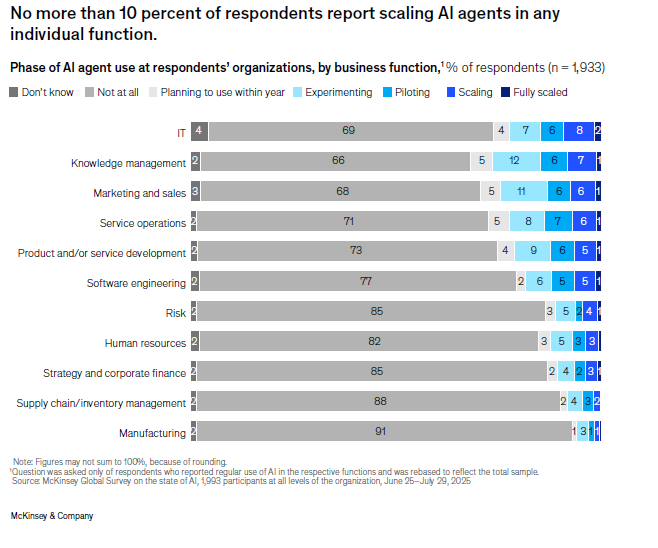

McKinsey & Company (Nov 2025). The State of AI: How Organizations Are Rewiring to Capture Value from AI Page 5 Exhibit 2.

McKinsey’s latest global research indicates that only 10% of organizations report scaling AI agents within any given function. Experimentation is widespread. Pilots are common. Enterprise-wide deployment remains selective.

As Don Shin, Founder & CEO of CrossComm, a consultancy with a 25+ year history of helping organizations leverage emerging technologies such as AI into their digital products and workflow, says

“Most organizations treat AI agents like a technology problem, but the challenge is actually an organizational one. The teams that stall between experimentation and execution almost always underestimate the same things: their data isn't as ready as they think, their people haven't been brought along for the ride, and nobody's properly defined accountability and the blast radius for when things go wrong.”

“Yes, getting agents into production involves tech- but a successful business outcome hinges on governance, change management, and finding the sweet spot between capability and safety.”

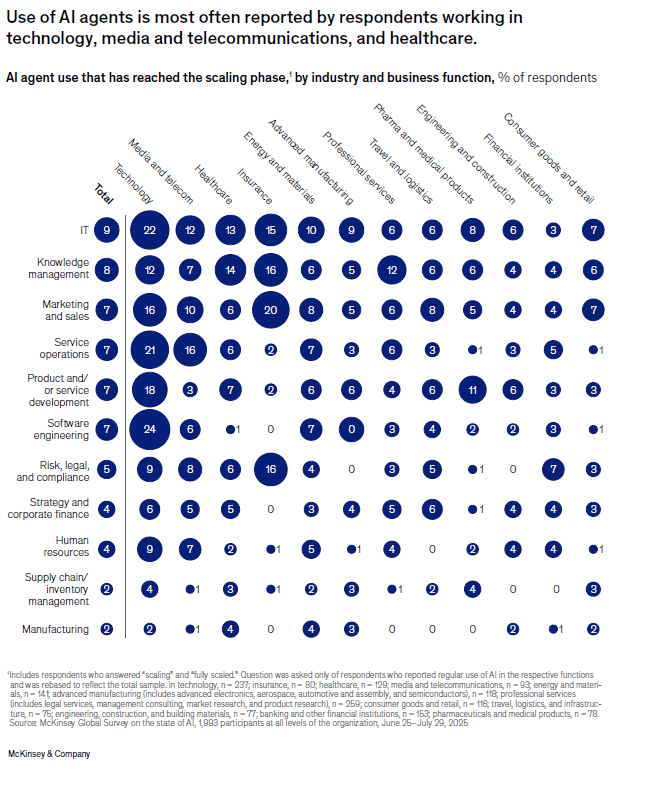

Selective Scaling Is a Structural Pattern

Agent-based systems appear most frequently in technology-driven sectors such as tech, media, telecommunications, and healthcare. Within organizations, IT and software-related functions report greater maturity than operational domains like supply chain, manufacturing, or corporate finance.

Source- McKinsey & Company (2025). The State of AI: How Organizations Are Rewiring to Capture Value from AI Page 6 Exhibit 3

Executive concerns as organizations move beyond pilots

Why Pilots Stall: The Structural Reality Behind Enterprise AI

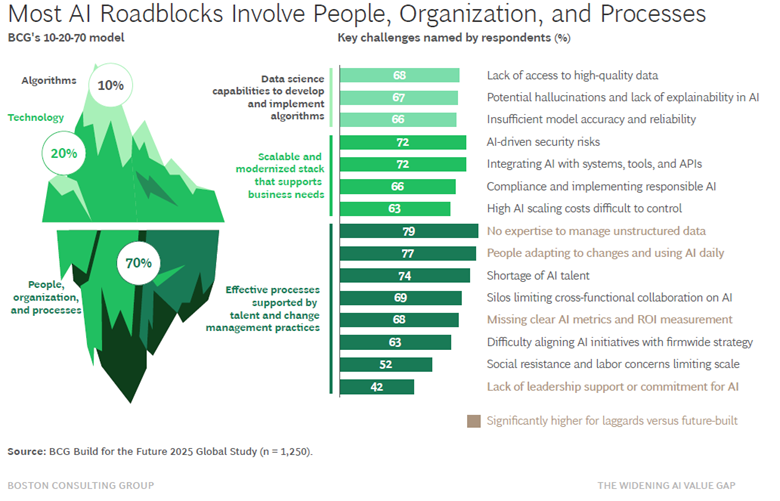

Boston Consulting Group’s (BCG) 10-20-70 framework offers a useful lens. Only about 10% of AI value creation comes from algorithms, roughly 20% from technology and infrastructure, and the remaining 70% from people, processes, and organizational alignment.

Source: Boston Consulting Group, 10-20-70 Framework for AI Value Creation, Sept 2025- The Widening AI Value Gap: Build for the Future 2025.

BCG’s 2025 global study confirms this imbalance. The most common barriers to scaling AI are not model limitations but organizational ones — fragmented data, integration challenges, siloed collaboration, unclear ROI measurement, talent shortages, and resistance to change.

Deloitte’s State of AI in the Enterprise: The Untapped Edge (2026) reinforces the same pattern. Despite widespread expectations for automation, 84% of companies have not redesigned jobs or workflows around AI capabilities, and fewer than half have significantly adjusted their talent strategies.

Without redesigning work itself, pilots rarely scale.

As Prasad Varahabhatla, Sr. Director, Process Engineering & AI Solutions at Cisco’s Automation & AI Center, observes:

“The Change Management activity for AI implementations is multifaceted. Once AI enters a process, it alters the process boundaries, necessitating a reevaluation of human roles. I notice that job design and new ways of working do not get the same TLC (Tender Loving Care) as the excitement about the new technology. Implementing AI without fundamentally changing work will dilute value realization and creates other undesirable consequences.”

A pilot can operate in isolation with curated data and limited scope. Production requires integration, security validation, governance, monitoring, and operational ownership. What succeeds in a controlled environment often struggles under enterprise complexity.

The real challenge is not the model. It is the organization.

Debunking the Common narratives shaping AI

Public narratives around AI tend to move faster than enterprise reality. Headlines amplify extremes — extinction, collapse, or instant transformation. It is worth examining a few of the most persistent narratives shaping today’s AI conversation.

Narrative: Software Is Dead, Agentic AI will replace Enterprise Applications

The sharp sell-off in software stocks — nearly 30 percent from peak — has fueled a new narrative: that AI agents will replace human “seats,” commoditize code, and ultimately erode traditional SaaS economics.

If AI can write software and execute workflows autonomously, the argument goes, the economic foundation of per-seat licensing begins to weaken.

History suggests caution before declaring extinction.

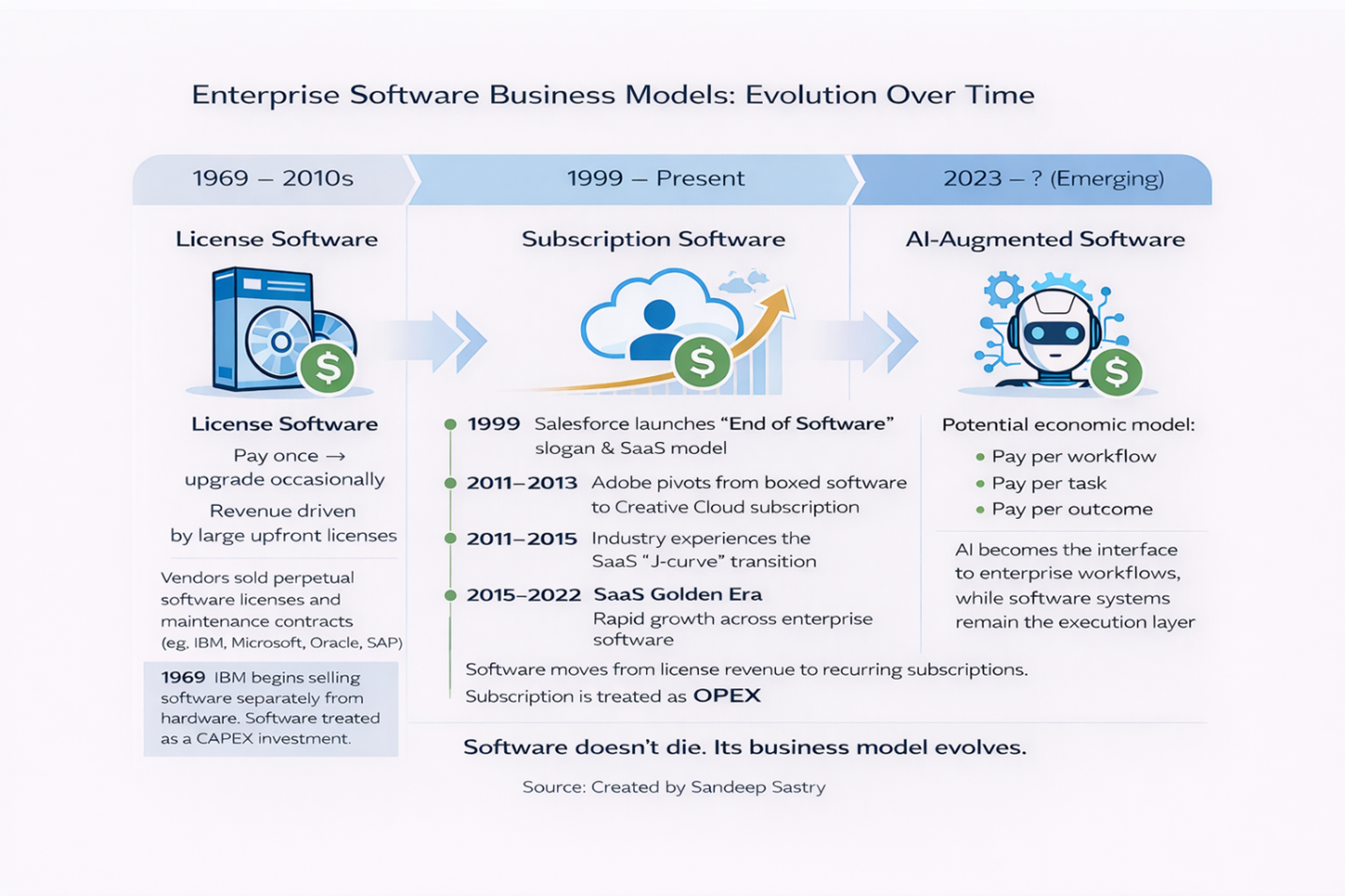

Enterprise software has already gone through multiple architectural and economic transitions.

In the early era of enterprise computing, software was typically sold through perpetual licenses, with organizations paying upfront and treating the purchase as capital expenditure. This model emerged after IBM’s 1969 decision to unbundle software from hardware and dominated enterprise IT for decades.

The next major disruption came in 1999, when Salesforce launched its SaaS platform with the now-famous slogan “End of Software.” The idea was that applications would no longer be installed locally but delivered through the internet as subscription services.

The transition unfolded gradually. Incumbents such as Microsoft, Oracle, and SAP continued selling license-based products for years while slowly adapting to subscription delivery models.

The real inflection point arrived between 2011 and 2015, when companies like Adobe pivoted from boxed software to subscription services such as Creative Cloud. This period produced what analysts often describe as the SaaS J-curve — a temporary revenue reset as companies shifted from upfront license revenue to recurring subscriptions.

By the mid-2010s, Microsoft’s launch of Office 365 accelerated adoption across the enterprise software industry, ushering in what many observers consider the SaaS golden era between roughly 2015 and 2022.

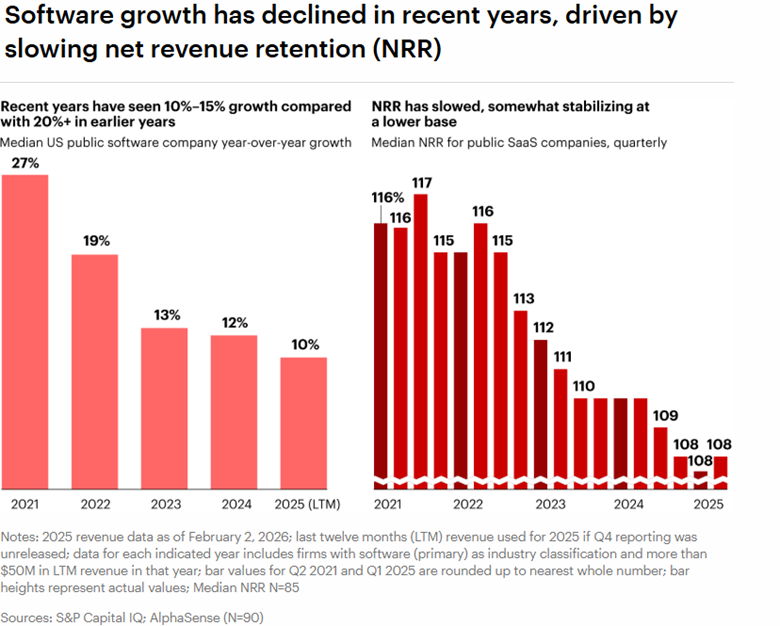

Since 2022, however, SaaS growth has slowed noticeably. Expansion within existing customers — long the engine of software growth — has weakened as enterprises consolidate vendors and moderate cloud spending after years of rapid adoption.

Source: Bain & Company, “Why SaaS Stocks Have Dropped and What It Signals for Software’s Next Chapter,” 2026

As the data shows, median growth among public software companies has slowed since the pandemic-era surge. Net Revenue Retention (NRR) — a key measure of expansion within existing customers — has declined from roughly 116–117 percent in 2021 to about 108 percent in 2025.

This shift reflects a maturing market rather than the disappearance of enterprise software.

What may be emerging instead is another evolution in the economic model.

If AI agents increasingly execute workflows across enterprise systems, pricing may gradually move away from simple per-user subscriptions toward consumption models tied to workflows, tasks, or measurable outcomes.

In that sense, the current debate about whether “software is dead” may echo earlier transitions in the industry. Applications rarely disappear. What changes is how software is delivered, consumed, and monetized.

Narrative: Big Tech’s Massive AI CapEx in anticipation of Rapid Enterprise Adoption

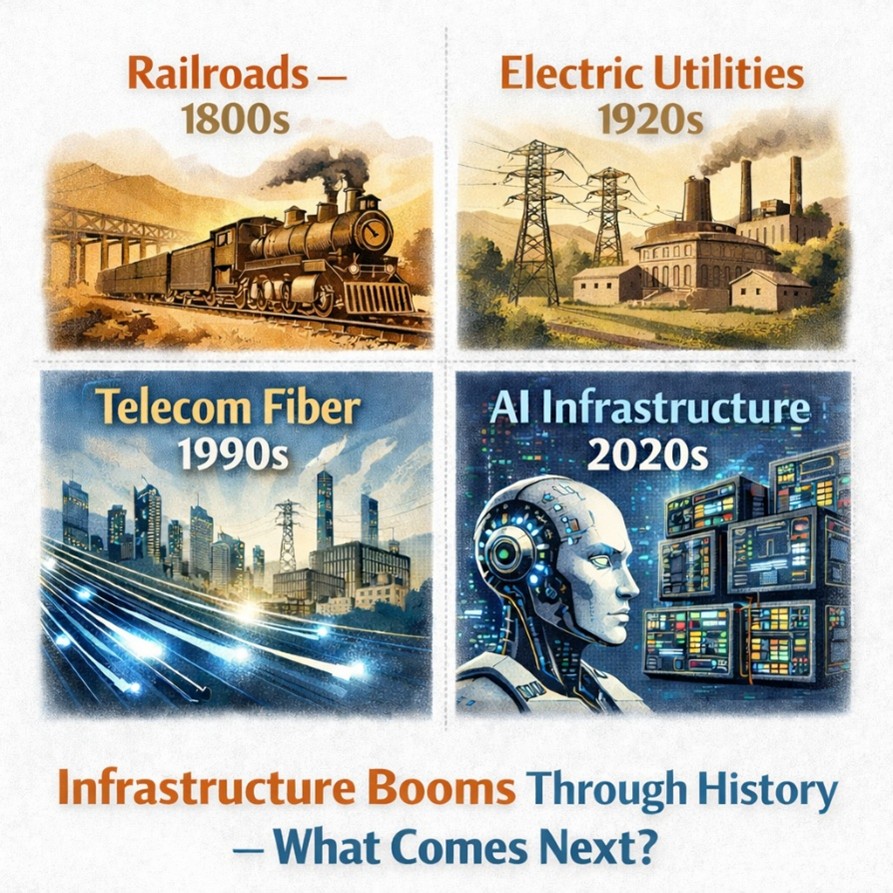

The scale of AI-related capital spending by Big Tech has led many to assume that enterprise adoption will accelerate uniformly. History suggests a more disciplined interpretation.

In the late 1990s, telecom companies such as WorldCom, Global Crossing, and Qwest raced to lay fiber as competitors rushed to build national networks. Capital flowed aggressively into infrastructure long before demand fully matured. When the dot-com bubble burst, overcapacity became visible. Several firms collapsed or went bankrupt.

Yet the infrastructure itself survived. Over time the industry consolidated, and the fiber networks built during that period eventually became the backbone of the modern internet.

Earlier infrastructure cycles followed similar patterns. Railroads in the 1800s and utility holding companies in the 1920s both experienced periods of aggressive expansion followed by consolidation.

Source- Created by Sandeep Sastry

In each case, capital moved first — often ahead of proven consumption — as firms positioned for advantage and responded to competitive pressure.

Another dynamic worth noting is how parts of the AI ecosystem are financing the buildout itself. Large technology firms are investing in AI startups that then spend heavily on their infrastructure. NVIDIA’s relationship with OpenAI, Amazon’s investment in Anthropic paired with cloud credits, and Microsoft’s integration of OpenAI with Azure illustrate how capital, infrastructure spending, and product adoption can become closely intertwined.

Accounting assumptions are also beginning to attract attention. High-performance GPUs evolve quickly, yet some companies depreciate these assets over five or six years, which can smooth near-term earnings if the economic life proves shorter.

Much of the current buildout has been funded from the substantial cash reserves accumulated by Big Tech over the past decade, but debt is beginning to supplement that spending. Amazon’s recent bond issuance is one example. Competitive pressure can quickly amplify infrastructure cycles once they begin.

AI infrastructure spending today reflects similar dynamics. Hyperscalers cannot afford to appear underinvested relative to peers. Competitive signaling influences capital allocation as much as current enterprise demand.

At the same time, the AI buildout is encountering practical constraints that receive far less attention than model breakthroughs. Supply chains for critical components — particularly high-bandwidth memory used in advanced AI chips — are tightening as demand surges. Large data centers also require enormous amounts of electricity and cooling, forcing utilities in several regions to accelerate grid upgrades or develop dedicated power arrangements for hyperscale facilities. In some cases, thousands of GPUs have already been delivered to data centers but remain idle while power infrastructure catches up.

Heavy investment signals long-term conviction. It does not guarantee synchronized adoption across industries and functions.

Infrastructure buildout and value realization rarely move at the same speed.

Another argument often made is that this technology cycle will move far faster than previous ones. There is some truth to that. AI capabilities diffuse rapidly because they are software-driven and delivered through cloud platforms, allowing millions of users to experiment almost instantly.

But enterprise adoption operates under a different set of constraints. Integrating AI into production systems requires data readiness, security validation, governance frameworks, and changes to how work is performed. Those organizational realities tend to move at a much slower pace than technology itself.

As a result, capability adoption may accelerate quickly, while enterprise value realization still unfolds over time. AI may spread rapidly as a capability, but enterprise transformation still moves at organizational speed.

Narrative: AI Will Replace Most Jobs in the Near Term

The dominant fear is rapid, large-scale job displacement. The data does not support that conclusion. Deloitte’s 2026 State of AI in the Enterprise reports that 84% of organizations have not redesigned jobs around AI, and fewer than half have meaningfully adjusted talent strategies. At the recent NC Tech Outlook for Tech 2026 event in Charlotte, Forrester projected that AI and automation may affect roughly 6% of jobs by 2030, with most of the impact coming through augmentation rather than elimination. They also noted that some AI-attributed layoffs may quietly reappear offshore or at lower cost structures — reflecting economic reallocation rather than wholesale job extinction.

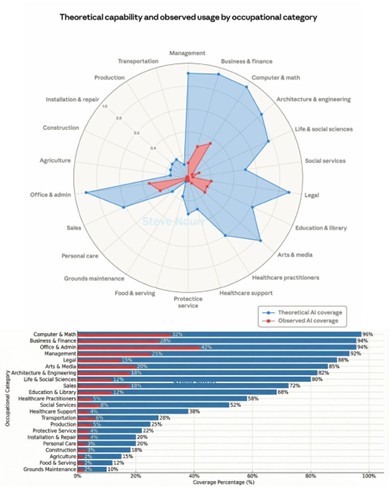

Recent research from Anthropic highlights another important dynamic: the gap between AI capability and real-world adoption. By analyzing millions of workplace interactions with its Claude model, the company introduced a metric called “observed exposure,” comparing the tasks AI could theoretically perform with the tasks where AI is actually used today. Even in highly exposed knowledge-work fields such as programming or research, real-world usage remains far below theoretical capability. The spider chart below illustrates this divide between AI’s technical potential and its current operational footprint.

Anthropic Economic Research (Mar 5 2026) Labor market impacts of AI: A new measure and early evidence. Courtesy Steve Nouri for representing in occupational category in bar graph

The research also has important limitations. Because the dataset is derived from Claude interactions, it primarily captures language-based and knowledge-work tasks, such as writing, coding, and analysis. Other forms of AI — including autonomous driving, robotics, and industrial automation — fall outside this dataset. For example, transportation appears near zero in the chart even though AI already plays a central role in autonomous vehicle systems and logistics optimization. The chart therefore reflects one layer of the AI economy rather than the full spectrum of AI deployment.

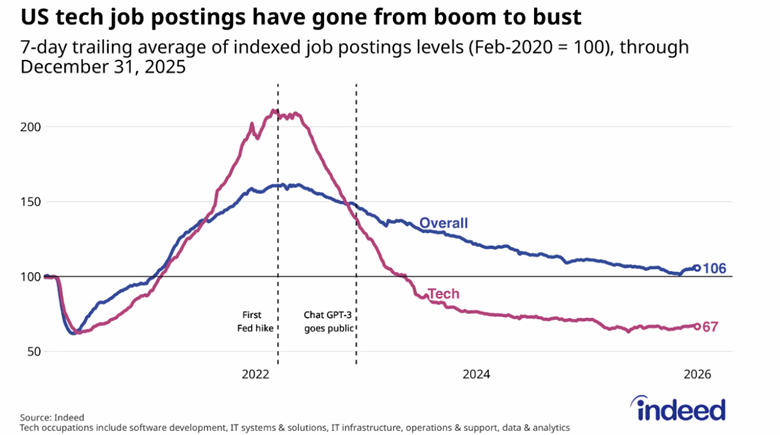

The broader labor market also reflects familiar economic cycles rather than sudden technological disruption. At the recent NC Tech Wilmington event, economist Ted Abernathy presented findings from an economic study commissioned by NC Tech examining technology employment trends.

Source- NC TECH Wilmington Event- Navigating Complexity, Uncertainty, & Change 2026 Outlook for Tech (Indeed Jobs)

The analysis showed that tech hiring surged during the pandemic-era expansion and peaked around 2022 before moderating. The chart above illustrates this shift clearly. Tech job postings rose sharply during the low-interest-rate period of 2020–2022 and then declined as monetary tightening began. Importantly, the slowdown appears tied more closely to macroeconomic conditions than to the emergence of generative AI. Hiring began cooling even before ChatGPT’s public release and continued as venture capital funding and startup formation slowed across the technology sector.

Taken together, the evidence points to a more measured reality: AI is reshaping tasks and productivity expectations far faster than it is replacing professions.

Narrative: AI Is Destroying College-Level Entry-Level Jobs

One of the most widely circulated narratives about AI is that it is rapidly eliminating entry-level jobs traditionally filled by recent college graduates. Headlines often point to hiring slowdowns in technology companies, fewer entry-level software roles, and growing uncertainty among new graduates entering the labor market. While these concerns deserve attention, history suggests the explanation may be more complex.

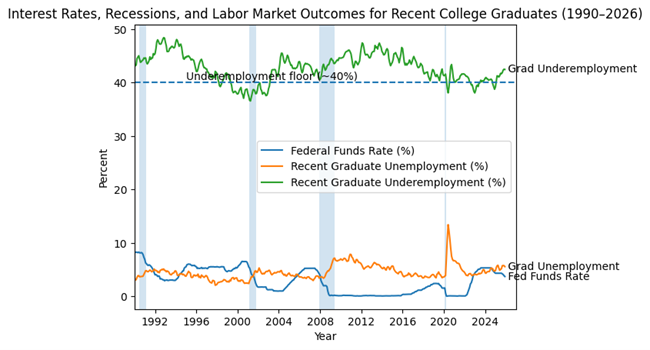

A look at the relationship between interest rates, economic cycles, and the labor market for recent graduates provides useful context.

Created by Sandeep Sastry Interest Rates, Recessions, and Labor Market Outcomes for Recent College Graduates (1990–2026) Sources: Federal Reserve (FRED), Federal Reserve Bank of New York, NBER recession dates.

A broader historical view suggests that weak hiring for recent graduates is not new. Periods of aggressive monetary tightening have repeatedly coincided with softer entry-level labor markets — visible in the early-1990s recession, the post-dot-com slowdown, the financial crisis, and the recent inflation-fighting cycle beginning in 2022.

Two observations stand out. First, underemployment among recent graduates rarely falls far below the forty-percent range, even during economic expansions. A significant share of graduates has long worked in roles that do not require a college degree — a structural feature of the labor market that predates generative AI.

Second, entry-level hiring in the technology sector is closely tied to the availability of capital. When interest rates rise, venture capital funding typically contracts, startup formation slows, and hiring of junior talent often becomes more cautious.

Higher borrowing costs also tend to shorten the planning horizon for many businesses. Firms become less willing to invest in training and development programs that may take years to pay off, and instead favor experienced hires who can contribute immediately. Seen through that lens, the recent softness in graduate hiring may reflect a familiar macroeconomic cycle rather than a sudden technological displacement driven solely by artificial intelligence.

Part of the anxiety surrounding AI and entry-level employment stems from the types of roles most visibly affected. Computer programming and software roles have historically been among the highest-paid entry-level positions for college graduates. Data from the Federal Reserve Bank of New York shows that computer science and computer engineering majors rank near the top of early-career wages. When generative AI appears capable of automating portions of coding and software development, the perceived threat is not just job loss — it is the potential disruption of one of the most attractive economic pathways available to recent graduates.

Yet over the longer term, the technology industry still depends on a steady pipeline of computer science and engineering graduates. Every major technology wave — from the internet to mobile to cloud computing — has ultimately increased demand for skilled technical talent. AI is unlikely to be different. Rather than eliminating the need for new engineers, it is more likely to change the tools they use and the skills employers expect.

For young graduates entering the workforce, the implication is not to avoid AI but to learn how to work with it. Those who understand how to leverage AI tools to write code faster, analyze data more effectively, and build new applications will likely become more valuable in the labor market, not less.

My thoughts: Where Enterprise AI is heading next

So where does this leave enterprise leaders thinking about AI today?

Every major technology cycle begins with experimentation, aggressive capital investment, and powerful narratives about how quickly everything will change. What follows is slower and more demanding: integrating the technology into real business processes, redesigning work around it, and proving measurable economic value.

That transition is now underway.

The organizations that will lead the next phase of AI adoption will not necessarily be those running the most pilots. They will be the ones embedding AI into core workflows, redesigning decision processes, and connecting the technology directly to measurable outcomes.

Access to models will not be the differentiator.

Execution will be.

I often return to Roy Amara’s observation:

“We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.”

That insight feels particularly relevant today.

In the short run, narratives move faster than enterprise reality. Markets extrapolate quickly. Expectations overshoot.

In the long run, however, the structural shifts compound.

AI will not transform enterprises overnight. But over time it will reshape productivity, cost structures, and competitive positioning across industries.

After watching several technology waves move through large enterprises over the past two decades, the pattern feels familiar: the excitement comes early, but the real benefits arrive much later.

About the Author

Sandeep Sastry is an enterprise strategy and technology leader with over two decades of experience across global organizations including Cisco, Chevron, and Pure Storage. His work centers on turning strategic intent into disciplined execution and measurable business outcomes — particularly as enterprises navigate AI adoption and large-scale transformation.

He writes about his perspectives on strategy, AI, sales and marketing effectiveness, customer value creation, capital markets, and leadership. More insights and perspectives can be found at www.sandeepsastry.com.

For his earlier 2024 perspective on Generative AI adoption, see:

GenAI: True Adoption in the Enterprise Today

https://sandeepsastry.com/genai-true-adoption-in-enterprise-today/

Interested in submitting a piece for the NC TECH blog?

NC TECH is always seeking fresh content and we love to feature our members and leaders as well as showcase your expertise and information. Visit our Marketing Toolkit page to submit Member Spotlights, Take 5 Executive Spotlights, Women Leading in Tech Profiles, and Guest Blogs.

For more information about sharing your news, contact Alex Taylor.